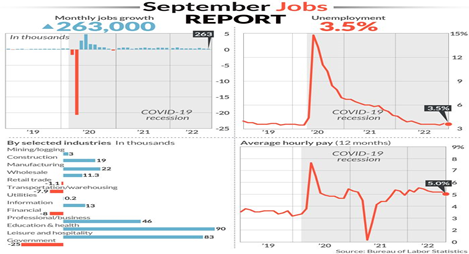

Every sector added jobs in October’s nonfarm unemployment report except mining, and the unemployment rate is still at a record low of 3.7 percent, even with the Fed promising to continue to raise interest rates.

“Total nonfarm payroll employment increased by 261,000 in October, and the unemployment rate rose to 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in health care, professional and technical services, and manufacturing.”

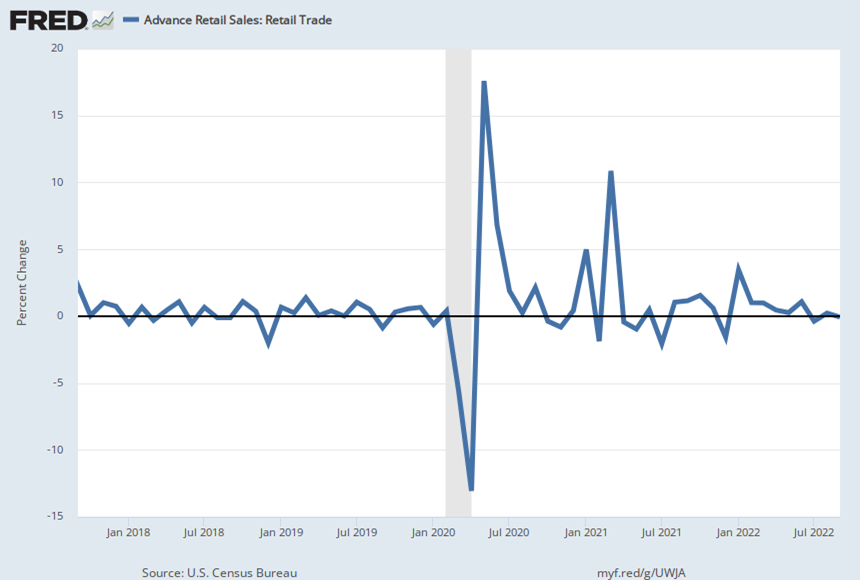

Why are businesses so busy that they see good times ahead rather than a looming recession? One answer is the U.S. economy grew 2.6 percent in the third quarter just reported due to exploding exports after two quarters of negative growth from the aftereffects of the pandemic, and record GDP growth in 2021.

I maintain it’s because we are still recovering from the pandemic, with two years of lock downs repressing demand. And 3 million working-age adults have not returned to the workforce, leaving businesses scrambling to find enough employees.

Americans are fully employed and there is a job for every American that wants one. We have almost twice as many job openings as jobs being created. More consumers want to travel and dine out, children are back in school, and supply chains have caught up in most sectors to meet the demand.

Education & Health y in the report added 79,000 jobs, followed by Professional/Business (39,000), Leisure and Hospitality (35,000) and Manufacturing (32,000) new jobs.

It’s incredible that Democrats haven’t trumpeted the need for more workers since it is immigrants that will fill those vacancies. Canada just announced they are welcoming new immigrants to fill their worker shortage, reports the Financial Times Christina Lu.

“Look, folks, it’s simple to me: Canada needs more people,” said Sean Fraser, the Canadian immigration minister. “Canadians understand the need to continue to grow our population if we’re going to meet the needs of the labor force, if we’re going to rebalance a worrying demographic trend, and if we’re going to continue to reunite families.”

Immigration shouldn’t be a political hot potato because of the U.S. worker shortage. Republicans are demonizing immigrants and opposing more workable immigration laws when immigrants are desperately needed to fill the 10 million plus job vacancies.

Nor should the Fed be pushing up the unemployment rate to cure inflation that they say is needed. They have it exactly backwards. More jobs create less pressure on rising wages and greater productivity, both tools that would bring down inflation, which is what happened with today’s unemployment report.

It showed wage increases are slowing from more than 5 percent to 4.7 percent in October, while more than 10 million jobs have come back since 2001 and the Biden presidency.

Then why so much political discontent when the current congress has just passed record-breaking legislation that will help the discontented populace that Nobel prize-winner Angus Deaton described in a recent Project Syndicate article:

“Although two-thirds of the adult US population does not have a four-year college degree, the political system rarely responds to their needs and has frequently enacted policies that harm them in favor of corporate interests and better-educated Americans. What has been “stolen” from them is not an election, but the right to participate in political decision-making – a right that is supposedly guaranteed by democracy. Viewed in this light, their efforts to seize control of the voting system are not so much a repudiation of fair elections as an attempt to make elections deliver some of what they want.”

Who has been delivering what red staters in particular say they want? Republicans have consistently opposed better health care insurance, such as Obamacare and increased Medicare spending, better labor laws, and a higher minimum wage that would most benefit the two-thirds of Americans Professor Deaton mentions.

In fact, government has never been the problem, though from President Reagan’s term onward Republicans have attempted to make it so.

Deaton concludes: “The less-educated Americans who are at a greater risk of dying early did not all vote for Donald Trump in 2016 and 2020; but many of them did. The overlap can be seen by tabulating “deaths of despair” – from suicide, drug overdose, and alcoholic liver disease – across counties and matching them to Trump’s share of the vote.”

We know how to solve this by making government the solution, as we did with the New Deal. And it is what the latest legislation has done—spending $trillions on longer term projects like infrastructure, climate change, and capping health care costs.

But, alas, its effects will take some time to benefit the most discontented Americans.

Harlan Green © 2022

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen