Ho hum. The U.S. economy was still fully employed in December. How boring! The St. Louis Fed (FRED) graph below shows the American economy has been at full employment since December 2021 when the unemployment rate first sank below 4 percent (to 3.9 percent).

And much of the hiring has been at state and local government levels because local governments are finally recovering from the COVID pandemic. That is the surest indicator of the beginning of a new uptick in the business cycle.

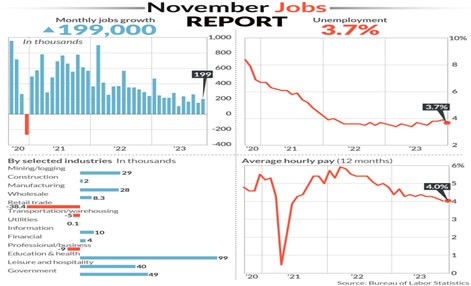

“Total nonfarm payroll employment increased by 216,000 in December, and the unemployment rate was unchanged at 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in government, health care, social assistance, and construction, while transportation and warehousing lost jobs.”

Average hourly wages of nonfarm private employees rose from 4.0 to 4.1 percent annually.

More good news is that factory orders have picked up, according to the Commerce Department, with new orders for U.S.-made goods increasing more than expected in November amid a surge in demand for civilian aircraft, government data showed on Friday.

Factory orders rose 2.6 percent after declining by 3.4 percent in October, the Commerce Department’s Census Bureau said. Orders climbed 0.7 percent on a year-on-year basis in November. And manufacturing, which accounts for 10.3 percent of the economy, is still being constrained by high interest rates. It should therefore pick up even more this year as interest rates decline further.

This is what is called a ‘soft landing’, I said when the unemployment rate dropped back to 3.7 percent in November. Government agencies at all levels added 52,000 new jobs in December – the biggest of any industry – to cap off a record year of hiring (i.e., total of 2.7 million new jobs in 2023), says MarketWatch’s Jeffry Bartash. “Altogether, government employment rose by 672,000 in 2023 and accounted for one-quarter of all new U.S. jobs created.”

So, what’s not to like about this jobs report? Maybe the Fed may now change its mind and not bring down interest rates so quickly, which could happen beginning this March? The evidence is becoming overwhelming that inflation is continuing to rapidly fall. Maybe Powell, et. al., may begin to worry that prices could plunge even more, which isn’t a good sign, since profits then begin to decline, a precursor to a recession.

I believe all the government hiring shows something else—a full blown recovery leading to a new business cycle and maybe what I’ve been calling a ‘Roaring Twenty-Twenties’. Such a ‘roaring’ recovery happened once before, a century ago at the end of the last pandemic that was caused by the Spanish Flu.

Then again, maybe a more boring economic recovery is in the works, with steady employment, wages continuing to rise more than inflation, and a majority of consumers admitting they are happy. Maybe a boring economy is good!

Harlan Green © 2024

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen