I have found support for my contention that the Fed should be done with raising interest rates and in fact drop them sooner rather than later, or we will see a full-blown recession.

Campbell Harvey, a Duke University finance professor best known for developing the yield-curve recession indicator in an interview on MarketWatch, says the Federal Reserve’s read on inflation is out of whack. And, as a result, the likelihood that the U.S. slips into a recession is increasing.

Why? Because, “Harvey said that if shelter inflation were normalized at around 1% or 1.5% (It’s longer term average), overall core inflation would measure closer to 1.5% or 2%. In other words, at — or substantially below — the Fed’s 2% target,” said MarketWatch’s Mark DeCambre.

Shelter costs are a lagging indicator; rental costs lag other costs because rental contracts typically change annually.

That is why there isn’t an accurate measure of today’s retail CPI inflation in particular, which is still positive.

The inflation rate is declining, which is called disinflation in economists’ terms. Yet if prices actually begin to drift into negative territory, it means we are in a recession. And prices have fallen precipitously since June 2022 when it reach 7 percent (see CPI graph above), though rising from its low of 3 percent to 3.7 percent over the past two months.

This is a huge plunge that signaled supply chains wasted little time in catching up to demand. Consumer prices ex-shelter were up +1.9 percent on a year-over-year basis in August, up from +1 percent in July, according to the Labor Department.

That is a verly low inflation rate, and skirting an outright deflationary spiral if the trend continues, as prices are wont to behave during business cycles.

Professor Harvey says he was right in predicting eight of the last recessions when the yield curve inverted. That is a time when the yield curves of the 10-year and 3-month fixed rates are inverted from their normal relationship. The 10-year yield is normally higher than the 3-month yield because it is for a longer term (i.e., 10 years).

But when reversed, banks cannot profit when they must lend money at a lower rate (many lone rates are based on 10-yr yield) than they borrow (e.g., at 1-3 mos.) when inverted, hence credit conditions are tightened, if it is prolonged.

And adding to the possibility of recession are the Fed’s credit-tightening rate hikes for more than one year.

It’s a dicey time when Fed officials seem to believe prolonged inflation is right around the corner. They just lowered their rate-reduction schedule from four to two times next year at last week’s FOMC meeting.

Nobel Laureate Paul Krugman has been saying this for months. His ‘supercore’ CPI with consumer prices excluding more volatile food, energy, used cars and shelter is at 2 percent.

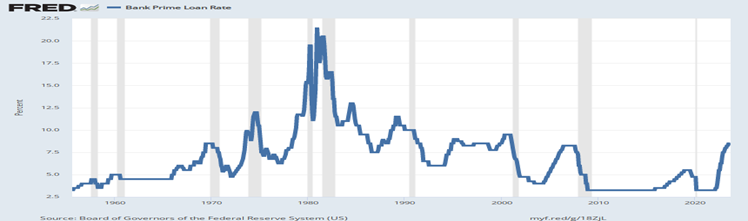

Yet we know what can happen when rate hikes are prolonged for too long. When former Fed Chairman Alan Greenspan and his Governors raised interest rates from 1 percent to 5.25 percent with 16 consecutive rate hikes from May 2004 to June 2006—the Great Recession followed.

Harlan Green © 2023

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen

{kind=link}