If I were the Fed Governors, I wouldn’t wait for inflation to drop further to begin lowering interest rates. The inflation rate has been falling steadily for more than a year and we might be in the midst of a deflationary spiral. Sound impossible? It could be if the Fed doesn’t see the writing on the wall.

The cost of living measured by the Consumer Price Index rose just 0.1 percent in November thanks to lower oil prices. Without food and gas prices, so-called core consumer prices rose a somewhat sharper 0.3 percent last month and matched the Wall Street forecast. And the annual rate of inflation slowed to 3.1 percent in November from 3.2 percent in the prior month, matching the lowest level since early 2021.

The next stage could be outright deflation, which nobody wants because it has spelled recession in the past. Why? Because the steep decline in inflation over a short period means a looming oversupply of things at the same time as sky-high interest rates, and that was the cause of past recessions.

The first indication of oversupply is gas prices, which are falling fast. As of Monday, the average national price for regular unleaded gasoline stood at $3.153 a gallon, down from $3.242 a week ago, and down from $3.376 a month ago, according to AAA.

The main reason is a weaker cost for oil, which is struggling to stay above $70 per barrel. The falling price comes just a week after OPEC+ announced voluntary production cuts of about 2 million barrels daily.

“Historically, crude oil tends to drop nearly 30 percent from late September into early winter with gasoline prices trailing the play,” said Andrew Gross, AAA spokesperson. “More than half of all US fuel locations have gasoline below $3 per gallon. By the end of the year, the national average may dip that low as well.”

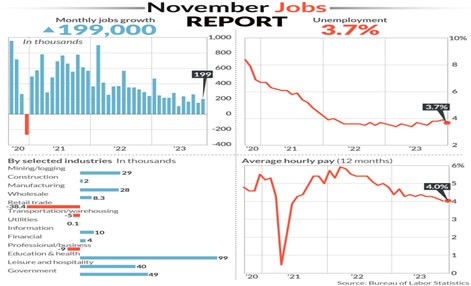

Inflation is falling fast with the 6-month CPI already down to 2.5 percent, yet unit wages are rising 4.0 percent annually in November’s unemployment report. So inflation today is being caused by higher rents and used cars, not oil prices as happened in the 1970s or rising wages.

We now know why inflation is falling. Nonfarm labor productivity is soaring, up 5.2 percent in the third quarter of 2023 as output increased 6.1 percent and hours worked increased 0.9 percent.

The increase in labor productivity is the highest rate since the third quarter of 2020, when productivity increased 5.7 percent. From the same quarter a year ago, nonfarm business sector labor productivity increased 2.4 percent.

The last time we approached bubble territory was an oversupply of housing in early 2000 that led to the housing bubble and Great Recession. Labor productivity was as high in Q1 2002 at 5.8 percent annually.

Under Fed Chairman Alan Greenspan, the Fed didn’t recognize the housing bubble until it was too late (In part due to lax supervision by the GW Bush administration Treasury and Greenspan’s Fed). In fact, he even encouraged homebuyers to take out adjustable-rate mortgages to prolong the housing market rally.

He then held the same 5.25 percent Fed Funds rate too long—10 months from August 2006 to June 2007—before the fed began to drop rates.

But by then it was too late. The Great Recession began in December 2007. Housing values had already begun to plunge due to a one-million-unit oversupply and the mortgages tied to them became worthless because they could no longer be serviced due to soaring mortgage rates that followed the Fed’s rate hikes.

Can this happen again? There is a pronounced undersupply of housing today with builders racing to catch up, so there is little danger of a housing bubble. Instead of looking backwards to the 1970s when oil shortages led to the inflationary spiral, the Fed should be focusing on possible oversupply today and falling prices as the production of things continues to ramp up.

There could be an oversupply in the industrial sector, for instance—of computer chips in particular as new factories begin to produce, and ordinary commodities as labor productivity stays high with AI and supply-chains continue to improve.

And let’s not forget the four bank failures to date due to the Fed’s rate hikes. The Fed should not forget the failure of Lehman Brothers and many other financial institutions that was also part of the Great Recession.

Harlan Green © 2023

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen